The Cost of Waiting to Buy a Home in San Diego in 2026

I get asked some version of this almost every week. Should I wait to buy in San Diego, or should I buy now? Most people asking are really wondering whether prices are about to fall, or about to run away from them. So instead of an opinion, here is the real cost of waiting to buy a home in San Diego, with actual numbers. I have been watching this market for almost twenty years, and the honest answer tends to surprise people.

How much does a home in San Diego actually cost right now

As of late spring 2026, the median sale price in San Diego County is about $922,000, according to Redfin. The part most people miss is that the number was up only 0.4 percent from a year earlier. Homes are selling around $583 per square foot, sitting about 23 days on the market, and there were 2,262 closed sales in May. You can track the local trends in my San Diego market reports. So this is a steady market, not a runaway one.

That matters for your decision. The story you have probably heard is that you need to buy immediately or get priced out. Over the past year, San Diego prices barely moved. The pressure to act this minute is lower than the headlines suggest. The real costs of waiting are quieter than that, and they are worth understanding before you decide either way.

Why San Diego feels so expensive

San Diego is expensive for reasons that are not going away. The coastline caps how far the desirable areas can expand, so there is only so much land near the water. Demand stays high because people want to live here, and that includes a steady stream of military, biotech, and remote workers. Add limited new construction and you get prices that hold their ground even when the rest of the country softens. None of that is a reason to panic-buy. It is a reason to understand that a long wait for some big San Diego price drop has not paid off for most people who tried it.

The cost of waiting, in real numbers

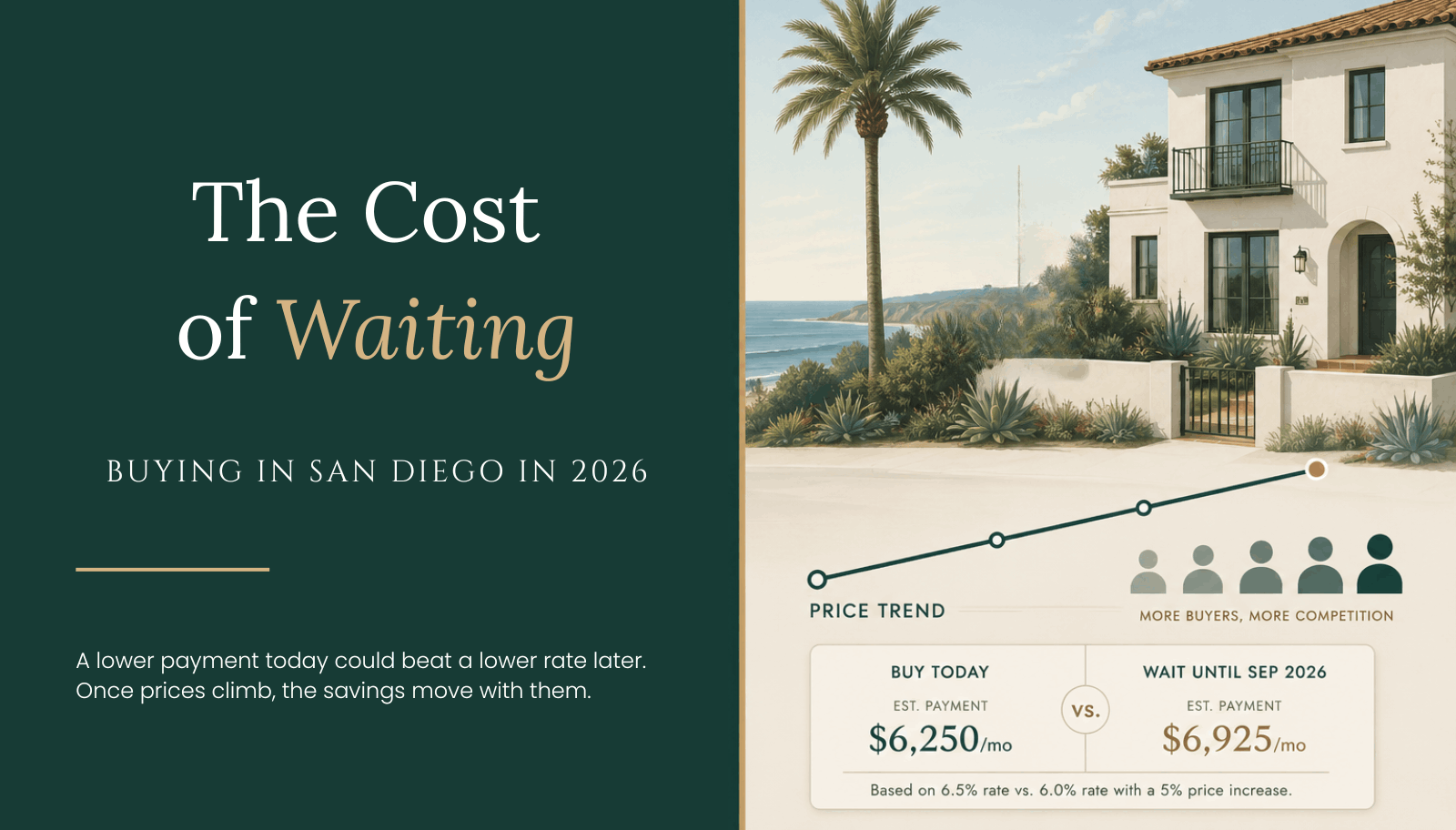

Let me put numbers to it. Take a $900,000 home, which is just under the county median. With 20 percent down, that is $180,000 down and a $720,000 loan. At a 30-year fixed rate near 6.5 percent, which is roughly where rates sit in June 2026 per Freddie Mac, the principal and interest payment is about $4,551 a month.

Here is the piece renters do not get. In the first 12 months of that loan, you pay about $54,600 toward it, and roughly $8,000 of that goes straight to principal. That $8,000 is equity. It is money you keep, sitting in your home, whether or not the market does anything at all. A year of renting builds you zero of that. So before we even talk about prices going up or down, waiting a year on this purchase costs you about $8,000 in forced savings you would otherwise be banking, plus a full year of rent that does not come back to you.

What waiting another year actually costs

There are three real costs to waiting, and I want to be honest about which ones are big and which are not.

Equity you do not build. As shown above, about $8,000 in principal paydown in year one on a $900,000 purchase. That grows every year you own, because more of each payment goes to principal over time.

Rent that does not come back. Whatever you pay in rent while you wait is gone. It builds your landlord's equity, not yours. Only you can run your own number here, but for most people renting near the coast it dwarfs the $8,000 figure above.

Rate and price drift. This is the one people fixate on, and it cuts both ways. If your rate ends up at 7 percent instead of 6.5 percent on that same loan, your payment rises about $239 a month, which is roughly $2,900 a year and close to $86,000 over the life of the loan. On the price side, if San Diego appreciated even 3 percent over the next year, your $900,000 home becomes $927,000 and your 20 percent down payment target climbs from $180,000 to about $185,400. That is roughly $5,400 more you would need just to hold the same position.

Now the honest caveat. San Diego prices rose only 0.4 percent over the past year, so the 3 percent figure above is a hypothetical, not a forecast. The case for buying now is not that prices are about to explode. The real cost of waiting is the equity you skip and the rent you cannot recover, with rate movement as the wild card nobody can predict. If you were waiting purely because you expect a big price drop, the recent data does not support that bet.

When waiting is the right call

Sometimes waiting is exactly right, and I will tell you so. If your income is not stable yet, if buying would leave you with no cash reserves, or if you might leave San Diego within the next two or three years, waiting usually wins. Buying makes the most sense when you plan to stay put long enough for ownership and equity to outrun your transaction costs. If that is not you yet, there is no shame in renting another year and saving. The goal is the right decision for your situation, not the fastest one.

Frequently asked questions

Is now a good time to buy a home in San Diego?

It depends far more on your situation than on the market. As of June 2026, San Diego prices are steady, up just 0.4 percent over the past year, and rates are near 6.5 percent. If you have stable income, your down payment, and plans to stay several years, the math generally favors buying over continuing to rent. If any of those is missing, waiting can be the smarter move.

What is the median home price in San Diego right now?

The median sale price in San Diego County is about $922,000 for the three months ending May 2026, according to Redfin. That is up only 0.4 percent year over year, so prices have been close to flat rather than rising sharply.

Will home prices in San Diego go down in 2026?

No one can promise a direction, and you should be cautious of anyone who does. Prices have been nearly flat, up 0.4 percent over the past year, and current forecasts are mixed. The safest approach is to base your decision on your own finances and timeline rather than on a prediction about where prices head next.

How much do I need to buy a $900,000 home in San Diego?

With 20 percent down, you would need $180,000 for the down payment plus closing costs, which commonly run another 2 to 3 percent. At a rate near 6.5 percent, the principal and interest payment on the resulting $720,000 loan is about $4,551 a month, before taxes and insurance. Lower down payment options exist and change these numbers, including VA loans for eligible buyers.

Are mortgage rates expected to drop in San Diego in 2026?

Forecasts do not call for a big drop this year. The Mortgage Bankers Association expects the 30-year rate to stay between 6.4 and 6.5 percent through the rest of 2026, and Fannie Mae projects about 6.3 percent by year-end. Planning around rates staying near where they are is more realistic than waiting for a large decline.

Let's talk through your numbers

If you have been sitting on the fence, the most useful thing you can do is run your actual numbers instead of guessing. I am happy to walk through your price point, your down payment, and what the monthly cost really looks like, with no pressure either way. Reach out anytime at Shirin@TheSDHome.com or call or text me at 858.750.5753, and we can figure out whether buying now or waiting makes more sense for you.

Categories

Recent Posts

GET MORE INFORMATION